Australia’s Housing Pipeline to 2029: BTR, Trade Constraints, and the HAFF Reality Check

June 30, 2026 | Investment

Date: June 2026

DISCLAIMER: This report discusses financial, tax, and investment-related topics. It is not tax advice, and the creators are not accountants. The content is for educational purposes only. You should consult your own investment-savvy accountant for personalized advice.

This combined report merges our analysis of Australia’s Build-to-Rent (BTR) sector and the broader 10-year housing pipeline, focusing tightly on the critical window to mid-2029. It examines project lead times adjusted for severe trade shortages, fact-checks the Federal Government’s Housing Australia Future Fund (HAFF) delivery versus its promises, compares how much affordable housing the private BTR sector delivers against the government’s own output, and highlights the structural tax advantages afforded to foreign institutional investors compared to everyday Australians, including the major 2027 changes to negative gearing and CGT. It concludes that the Government is quietly shifting social housing off its own books onto private and foreign corporations, and argues for reconsidering a scheme like NRAS to give ordinary Australians a leg-up instead.

1. The Total Housing Pipeline and Trade Constraints

Australia’s attempts to build its way out of the housing crisis are failing to gain traction. Based on the average of the last four years, the nation completes approximately 175,300 new dwellings per year . Holding this average flat would deliver roughly 1.75 million homes over the next decade.

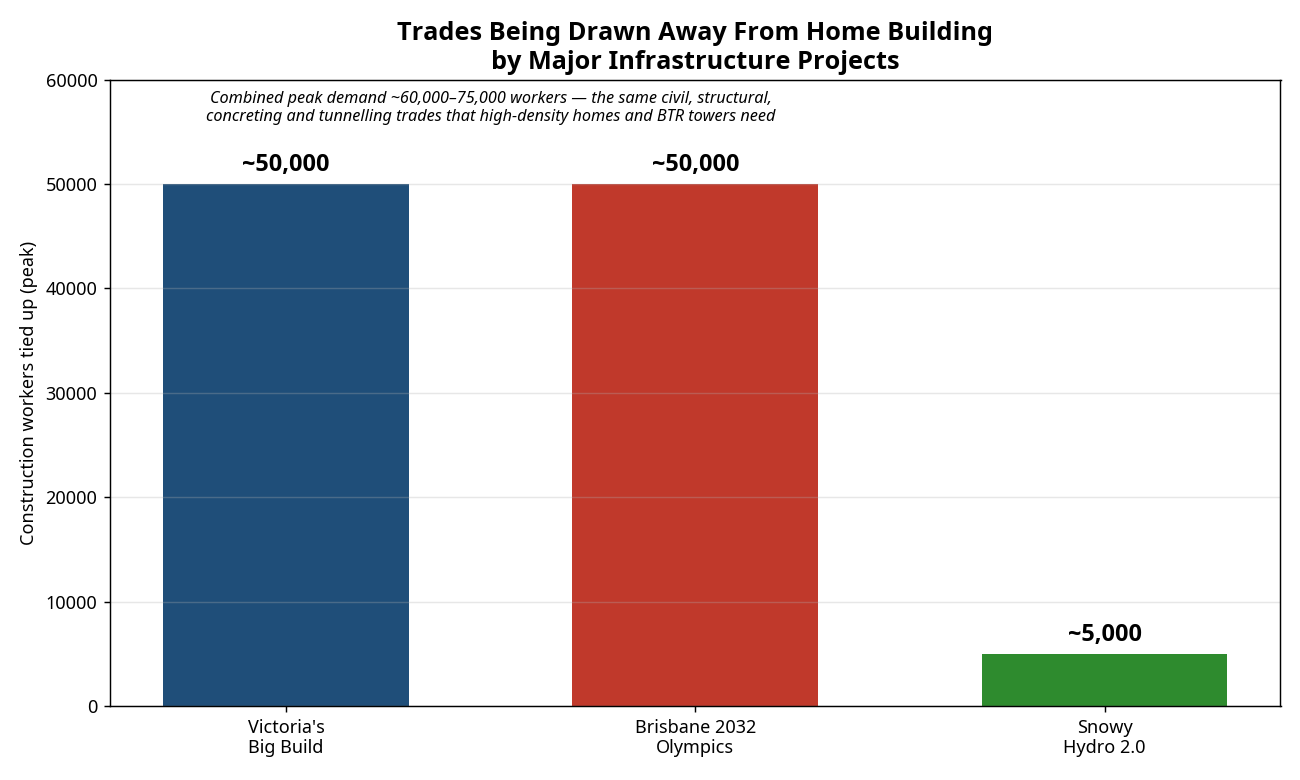

However, a straight-line average is unrealistic. The ability to build is heavily constrained by a critical shortage of construction labour. Infrastructure Australia projects that the national construction workforce shortage will reach a peak of 300,000 workers by 2027 .

This shortage is severely exacerbated by concurrent mega-projects that are directly absorbing the tradespeople needed to build homes. The scale of this labour diversion is substantial:

| Major Project | Workforce Tied Up | Investment / Scale |

| Victoria’s Big Build | More than 20,000 working directly on projects, with industry figures citing over 50,000 Victorians across the program (Metro Tunnel, North East Link, Suburban Rail Loop, Level Crossing Removals). Every 100 direct jobs support another ~206 indirect jobs . | Largest infrastructure program in the nation’s biggest housing state |

| Brisbane 2032 Olympics | Projected peak shortage of up to 50,000 construction workers in 2026–2027; the athletes’ village and main stadium are now under construction . | Over $11 billion in venues/transport, within a ~$200 billion Queensland pipeline |

| Snowy Hydro 2.0 | Approximately 5,000+ at peak workforce on a single remote project, drawing tunnelling, civil and structural trades . | Part of a ~$36 billion national utilities/energy pipeline |

Taken together, these three programs alone are consuming on the order of 60,000–75,000 workers at their peak, the bulk of them the very civil, structural, concreting and tunnelling trades that high-density residential and BTR towers also depend on. Because infrastructure projects generally pay more and offer longer job security than home building, residential construction consistently loses this competition for labour. This is the mechanism that pushes home completions below the four-year average precisely when demand (driven by migration) is rising.

When adjusted for this worker drain during the peak 2026–2029 period, the realistic 10-year projection drops to approximately 1.67 million homes a loss of over 80,000 homes to trade competition, falling roughly 30% short of the National Housing Accord’s target. If migration continues to rise, this supply shortfall will place further upward pressure on both rents and home prices.

2. Fact-Checking the HAFF: Promised vs. Delivered

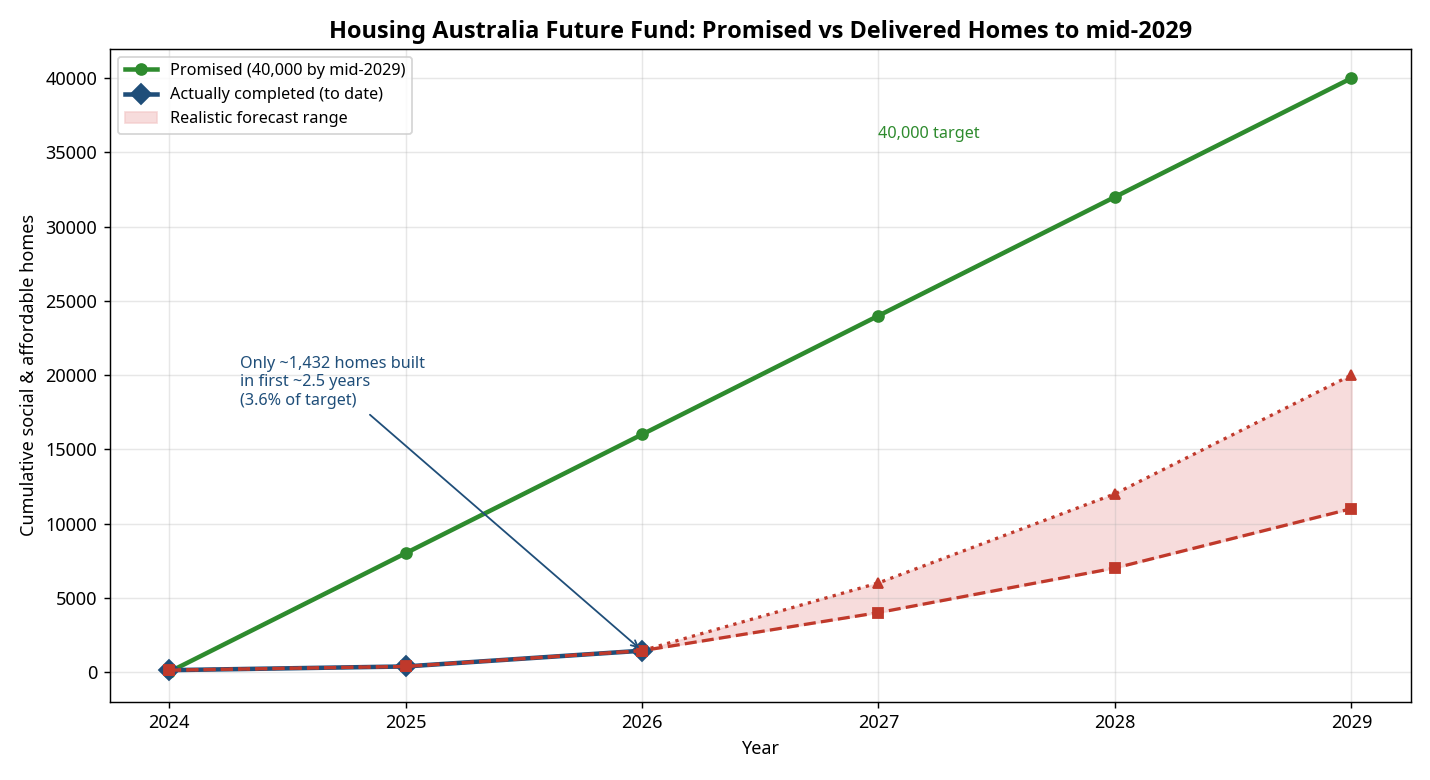

The Federal Government established the $10 billion Housing Australia Future Fund (HAFF) with a headline promise to deliver 40,000 social and affordable homes by mid-2029 (originally stated as 20,000 social and 10,000 affordable, later expanded) .

The Delivery Reality

Only around 300 homes had been built over the last two years to early 2025. As the program has progressed, the numbers have grown slightly, but remain alarmingly low relative to the target.

•As of late 2025: Only 889 homes had been completed .

•As of May/June 2026: Approximately 1,432 homes have been completed .

•Under Construction: While another ~9,500 are listed as “under construction,” industry bodies note this can mean anything from a poured slab to a cleared block of dirt .

To reach the 40,000 target by mid-2029, the HAFF must deliver roughly 8,000 homes per year over its five-year lifespan. Roughly two and a half years in, it has delivered just 1,432 homes, only 3.6% of the target. The program is currently the subject of a performance audit by the Australian National Audit Office .

3. Build-to-Rent: Affordable Housing Share

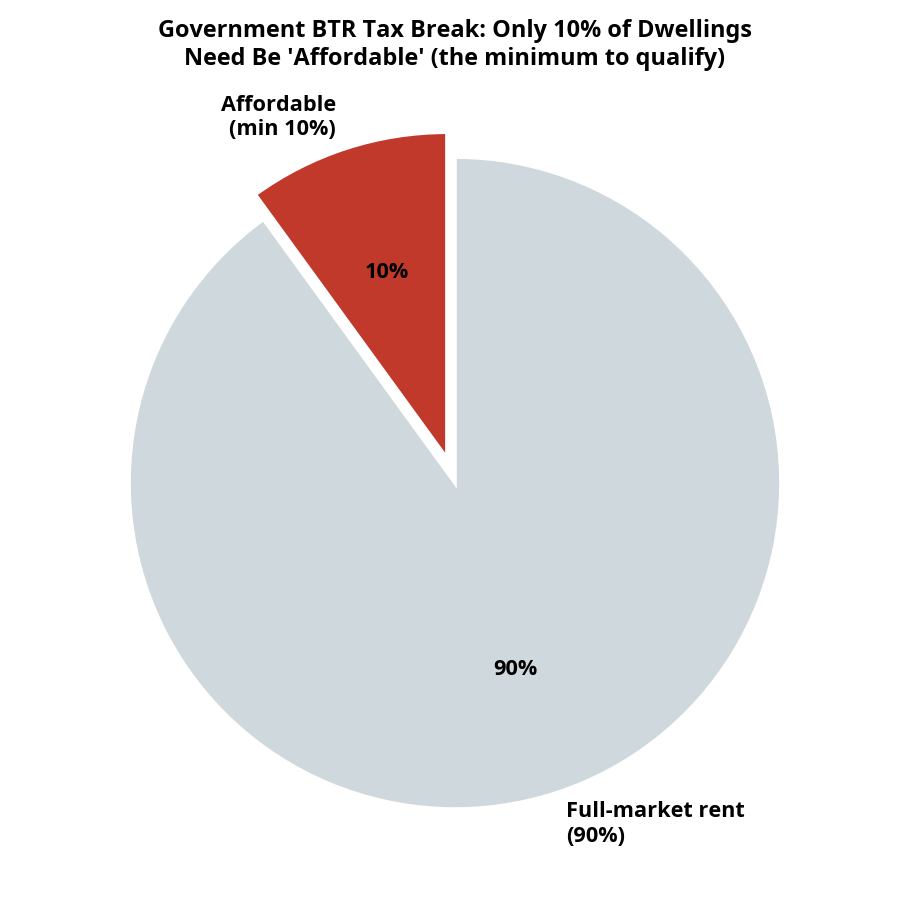

To stimulate the BTR sector, the Federal Government introduced specific tax concessions. However, to access these lucrative tax breaks, the government mandates that a specific percentage of the development be dedicated to affordable housing.

Under the legislation, at least 10% of the dwellings in an eligible BTR project must be designated as “affordable dwellings” .

These dwellings must have rent capped at 74.9% or less of the market value and be leased to tenants meeting specific income thresholds . Because the legislation sets the requirement at a minimum of 10% to trigger the tax break, the vast majority of developers model their financial feasibility on exactly 10%. This means that across the BTR pipeline, 90% of the dwellings built with government tax assistance remain at full market rent.

4. Who Is Really Delivering Affordable Housing? Government vs. Build-to-Rent

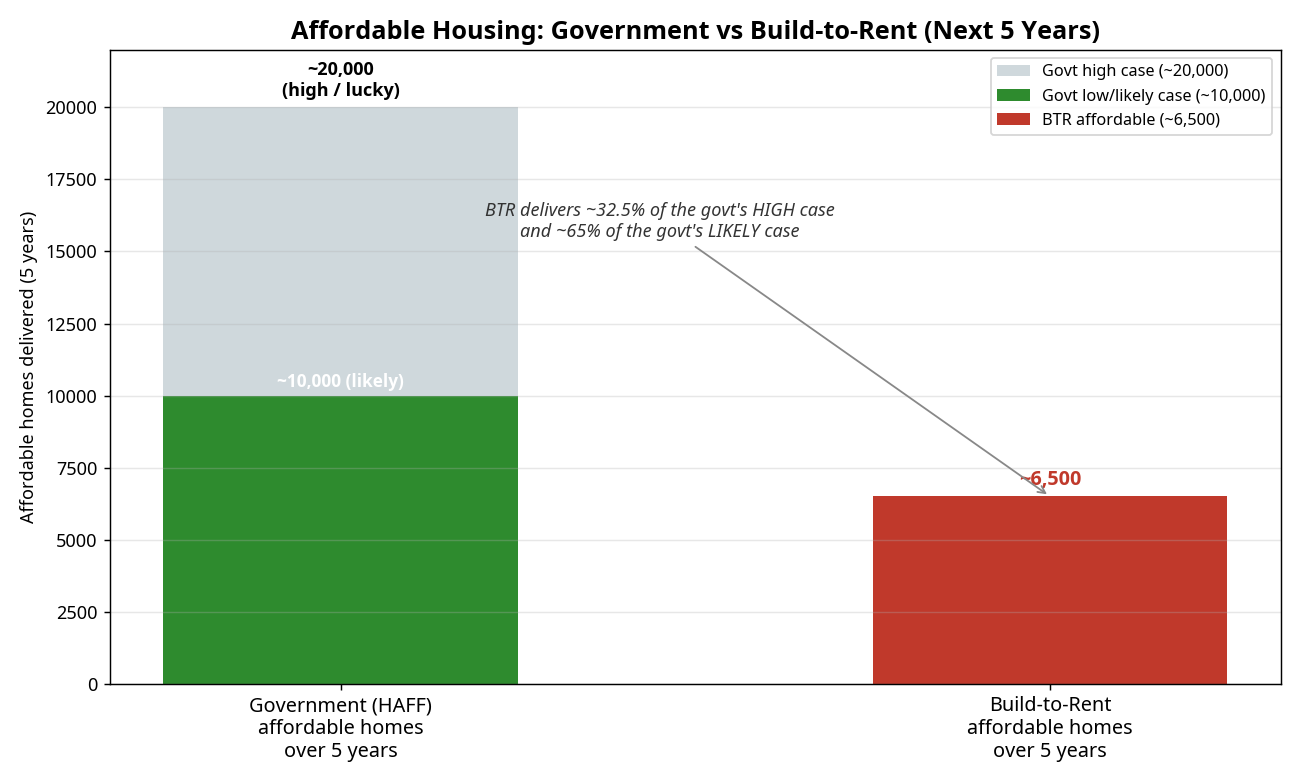

When the affordable-housing output of the two systems is placed side by side over the next five years, a striking picture emerges. The Government’s HAFF program is targeting somewhere between a realistic low of around 10,000 and an optimistic “if they get lucky” high of around 20,000 affordable homes over the period and, as the delivery record above shows, the high case is highly unlikely to be met. Meanwhile, the Build-to-Rent sector, delivering its mandatory 10% affordable component on a realistic completions pipeline, is on track to produce roughly 6,500 affordable homes over the same five years.

| Provider | Affordable Homes (5 years) | Notes |

| Government (HAFF) — likely | ~10,000 | Realistic low case, consistent with the current ~1,432 delivered run-rate |

| Government (HAFF) — “if lucky” | ~20,000 | Optimistic high case, unlikely on current trajectory |

| Build-to-Rent (10% mandate) | ~6,500 | Private/foreign-funded, delivered via the 10% affordable floor |

On these numbers, the privately-funded Build-to-Rent sector is set to deliver an amount of affordable housing equal to between roughly 32.5% (against the government’s lucky high case) and around 65% (against the government’s likely case) of what the Federal Government itself manages to put on the ground.

The Quiet Shift: Social Housing Moving Off the Government’s Books

This comparison reveals a significant policy shift. The Federal Government is effectively transferring the responsibility for affordable and social housing off its own balance sheet and onto private business. Rather than directly building and owning housing stock, as governments did for decades, it is now relying on tax concessions to induce private and overseas-owned corporations to deliver a slice of affordable product as a by-product of profit-driven, market-rate developments.

The deeper concern is who is being given the leg-up. Instead of empowering ordinary Australian “mum-and-dad” investors to build wealth through property and supply rental housing, the very investors who are about to be hit by the 2027 negative gearing and CGT changes described below, the policy settings are channelling the most generous concessions to large institutional and foreign players such as BlackRock and other multinational capital. In effect, the nation is outsourcing a core public responsibility, and a share of the long-term wealth that flows from it, to multinational corporations rather than its own citizens.

A Better Path: Reconsider and Reinstate NRAS

There is an Australian precedent that worked. The National Rental Affordability Scheme (NRAS), introduced in 2008, paid an annual incentive to investors and community housing providers who built new dwellings and rented them to low- and moderate-income tenants at at least 30% below market rent for ten years . Crucially, NRAS was open to ordinary investors, not just billion-dollar institutions, it gave mum-and-dad investors a genuine leg-up to grow wealth through property while simultaneously expanding the affordable rental pool.

NRAS is now winding down, with all remaining dwellings exiting the scheme by June 2026, stripping more than 4,500 affordable rentals out of the system in its final year alone . Reintroducing and extending a modernised NRAS, learning from its earlier administrative shortcomings, would offer a powerful alternative: it would help everyday Australians build wealth through property, keep more of the nation’s housing wealth in domestic hands, and grow affordable supply, rather than selling out the nation’s wealth to multinational billion-dollar corporations.

5. Tax Concessions: Foreign Giants vs. Mum-and-Dad Investors

The Australian BTR sector is heavily reliant on overseas institutional capital, with more than 50% of the national pipeline backed by foreign investors . Global asset managers like BlackRock, alongside US real estate giants such as Greystar and Sentinel, are increasingly active in the Australian residential space .

The tax concessions designed to attract these foreign institutional players operate through Managed Investment Trusts (MITs) and differ fundamentally from the tax settings available to ordinary Australian “mum-and-dad” property investors.

| Feature | Institutional BTR Developer (via MIT) | Ordinary Australian Citizen Investor |

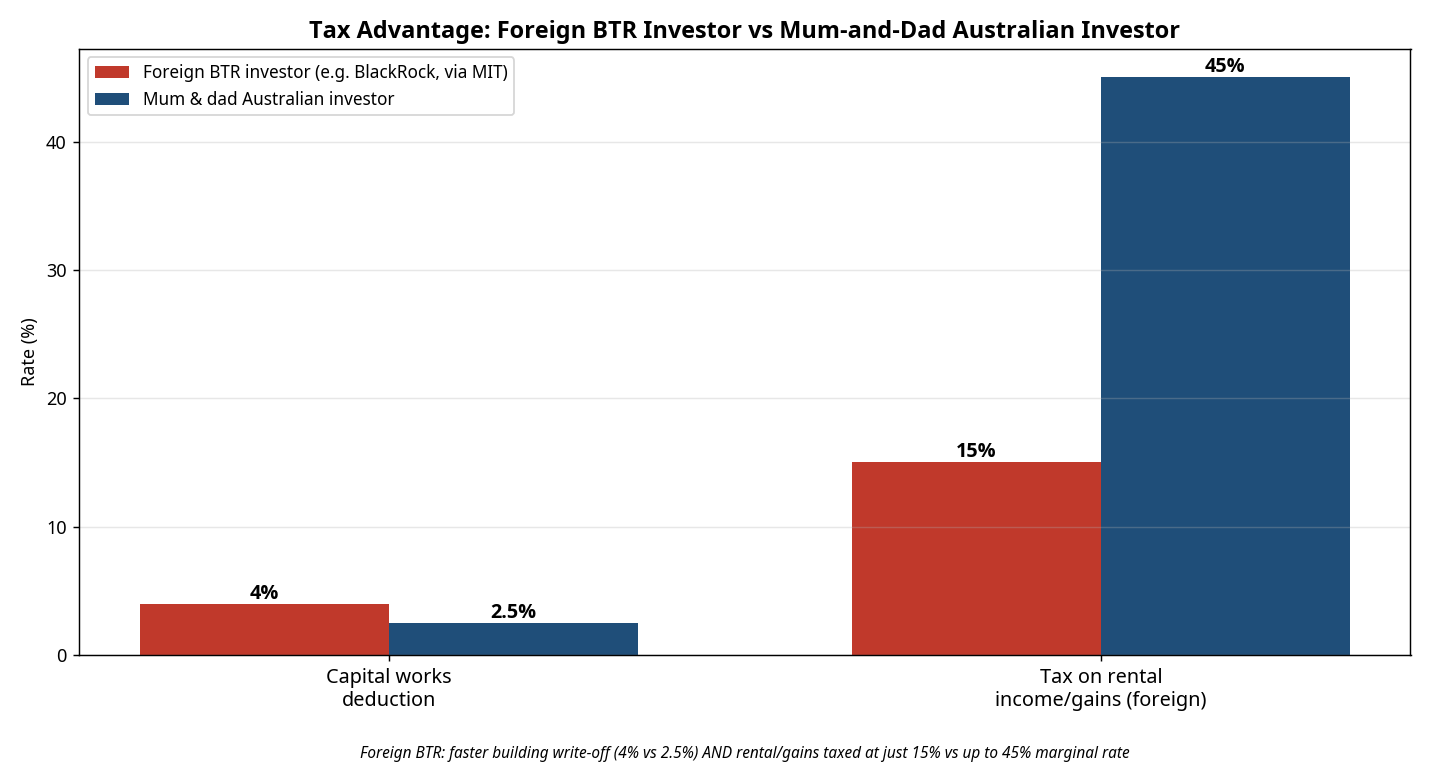

| Capital Works Deduction | 4% accelerated depreciation per annum . | 2.5% standard depreciation per annum . |

| Income Tax / Withholding | 15% concessional final withholding tax on rental income and capital gains for foreign investors (reduced from 30%) . | Taxed at the individual’s marginal income tax rate (up to 45% + Medicare levy). |

| Capital Gains | Captured under the 15% withholding rate for foreign MIT investors . | Eligible for the 50% Capital Gains Tax (CGT) discount if held for over 12 months (changing from 2027 please see below). |

| Losses / Gearing | Ring-fenced within the corporate/trust structure. | Eligible for Negative Gearing against personal wage income (restricted from 2027 please see below). |

Key Distinction: The BTR concessions are structurally inaccessible to ordinary citizens. They require a minimum development of 50 dwellings held under single ownership for at least 15 years . While ordinary citizens benefit from negative gearing and the 50% CGT discount, foreign institutional investors in BTR benefit from a halved withholding tax rate and faster depreciation of building costs.

The New 2027 Rules for Mum-and-Dad Investors

The playing field for ordinary Australian investors is about to become significantly harder, while the BTR sector is explicitly carved out and protected from the changes. In the 2026–27 Federal Budget (announced 12 May 2026), the Government legislated two major reforms that take effect from 1 July 2027 :

The first reform replaces the 50% Capital Gains Tax discount with cost-base indexation and a 30% minimum tax on net capital gains for assets held more than 12 months. This applies broadly to all CGT assets held by individuals, trusts and partnerships, not just housing. Gains accrued before 1 July 2027 keep the old 50% discount, but gains accruing afterwards fall under the less generous indexation-plus-minimum-tax regime .

The second reform restricts negative gearing to new builds. From 1 July 2027, net rental losses on established residential properties acquired after 7:30pm on 12 May 2026 can no longer be deducted against salary and wage income, only against other rental income or property capital gains (with unused losses carried forward) . Properties bought before that cut-off are grandfathered under the current rules.

Crucially, the legislation exempts new builds, widely held trusts, superannuation funds, and build-to-rent developments from the negative gearing restriction . Investors in new residential property may also choose between the old 50% CGT discount and the new indexation method. The net effect is a widening gap: the everyday Australian buying an existing home to rent out loses both the full CGT discount and the ability to negatively gear against wages, while the large institutional and foreign-backed BTR players retain their concessional 15% tax treatment and are specifically shielded from the negative gearing crackdown.

DISCLAIMER: This report discusses financial, tax, and investment-related topics. It is not tax advice, and the creators are not accountants. The content is for educational purposes only. You should consult your own investment-savvy accountant for personalized advice.

References

[1] Australian Bureau of Statistics, Building Activity, Australia, Oct 2025.

[2] Infrastructure Australia, 2025 Infrastructure Market Capacity Report, Nov 2025.

[4] MDPI, Rental Housing Supply and Build-to-Rent Conundrum in Australia, 2024.

[5] Housing Australia, Funding under the Housing Australia Future Fund, 2026.

[6] The Good Builder, 10 Billion, 1,432 Homes: What the HAFF Has Actually Delivered, Jun 2026.

[7] Australian Taxation Office (ATO), Build to rent development tax incentives, Feb 2026.

[8] BDO Australia / Altus Group pipeline analysis, Nov 2025.

[9] S&P Global, Build To Rent: A Credit Perspective On Australia’s Housing Future, Jul 2024.

[10] Snowy Hydro, Snowy 2.0 Overarching Factsheet, May 2026; Victoria’s Big Build, About Us, 2026.

[11] Baker McKenzie, Australia Budget Bites — CGT Discount and Negative Gearing, May 2026.

[12] Australian Taxation Office (ATO), Reforming negative gearing and capital gains tax, 2026.

[13] Department of Social Services / Wikipedia, National Rental Affordability Scheme (NRAS), 2026.

Recent Posts

We hope that you have found Australia’s Housing Pipeline to 2029: BTR, Trade Constraints, and the HAFF Reality Check helpful.

Click here to contact our expert team of Queensland Buyer's Agents.

Don’t forget to follow our buyer's agents team on Facebook or LinkedIn!